Approach to Real Estate Holdings for Asset Optimization (Asset Governance Policy)

The Yamato Group regards the sustainable enhancement of corporate value through improved return on capital as a key management priority, and is actively working to strengthen its balance sheet management. As part of these efforts, we hereby disclose the overall framework of Yamato Group’s real estate strategy, together with the evaluation process for our assets owned.

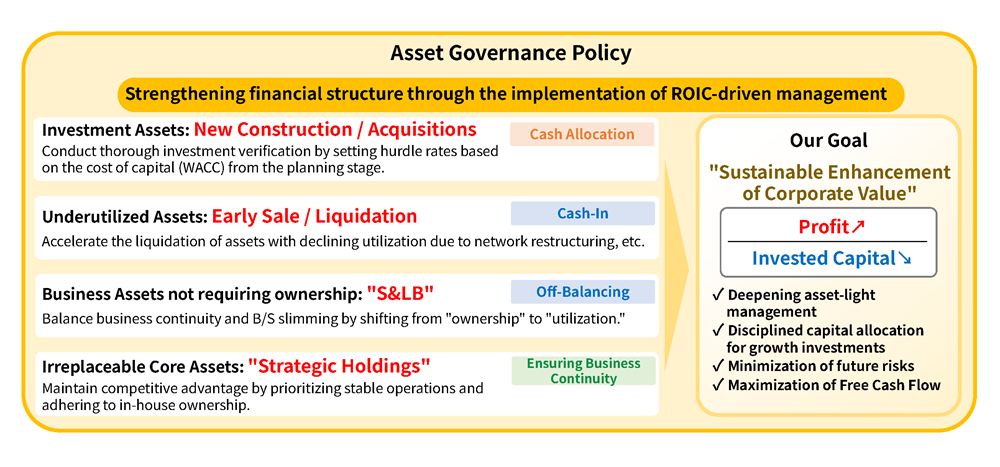

1. Basic Policy: Transition to "Asset-Light Management" ~ Completion of the Disposal of Non-Business Asset and Transition to the Next Phase ~

The Yamato Group is promoting “asset-light management,” seeking to balance the minimization of risk with the maximization of return on capital, based on ROIC (Return on Invested Capital) management. The streamlining of assets, which involved monetizing non-business real estate and other assets, was completed as of the fiscal year ended March 31, 2026. Going forward, we will transition from the previous phase—centered on monetizing non-core assets—to a phase where we further deepen our “asset-light management” in line with our core business strategy. In order to transform the business portfolio, Yamato will continuously execute a “comprehensive review with no sacred cows” of our asset portfolio from scratch, and establish a cycle that optimally allocates the capital generated toward disciplined growth investments—such as the expansion of business for corporates—and shareholder return through measures such as flexible and timely share buybacks.

Overview of Asset Governance Policy

2. Yamato’s Original Evaluation Framework

To achieve both the maximization of return on capital and the stability of business operations, we will go beyond the conventional framework of income and expense management, and rigorously evaluate and verify the rationale of our holdings based on the alignment with our management strategy and return on capital using the following two axes:

(1) Finance Axis (Contribution to financial performance and return on capital)

Quantitatively evaluate the investment profitability of each property, and the positive impact on financial metrics resulting from liquidation.

- Contribution to ROIC (Return on Invested Capital): Set a hurdle rate based on the cost of capital (WACC) and verify whether the asset is generating a return on capital that exceeds this rate

- Evaluation of Net Present Value (NPV) associated with liquidation: Compare and verify the one-off cash inflow generated by disposal or liquidation, against future rent obligations etc. associated with sale-and-leaseback (S&LB) transactions, using the cost of capital as a benchmark

- Comparison of ROIC before and after liquidation: Judge based on whether the ROIC of the facility can be maintained or improved following liquidation

(2) Business Axis (Business continuity and strategic value of the facility)

Evaluate whether the subject facility possesses irreplaceable functions as a pivotal node within our nationwide network—beyond its value as a standalone facility—and whether it is directly linked to our business competitiveness.

- Compatibility with Capital Expenditures: Verify whether automation equipment and buildings are structurally integrated, and whether in-house ownership ensures the flexibility and agility required for future large-scale automation investments (the introduction of robotics and material handling equipment, etc.), thereby contributing to the maximization of "earning power" in response to labor shortages and other challenges.

- Difficulty of replacement and reinvestment efficiency: For facilities where multiple Group functions (such as customs clearance, bonded warehousing, and value-added networking services) are highly integrated, compare the reinvestment costs associated with relocation or replacement against the cash inflows generated by liquidation, to evaluate medium- to long-term cash generation capacity.

- Assess burden of maintenance investments: Verify whether the costs of future major repairs and maintenance etc. will pressure profitability.

3. Asset Portfolio Classification and Execution Policy

Based on the evaluation framework described above, classify all real estate owned into the following three categories and execute optimal reorganization.

| Category | Evaluation results and characteristics | Execution policy |

|---|---|---|

| 1. Early disposal and monetization (Non-business and underutilized assets) |

Assets such as non-business real estate that have become less utilized due to network restructuring, and are tying up capital | In principle, prioritize early monetization through disposal and allocate the proceeds to growth investments and shareholder return |

| 2. Strategic liquidation (Assets eligible for S&LB) |

Assets that are necessary for business continuity, but do not necessarily require ownership by Yamato | Utilize S&LB and other approaches to shift from ownership to usage, thereby achieving both business stability and a lighter balance sheet |

| 3. Strategic ownership (Critical core assets) |

Assets in which the building and equipment are highly integrated, making it difficult to replace, and where in-house ownership leads to business competitiveness | Prioritize stable business operation, and protect our competitive advantage over the mid-to-long term by continuing ownership |

- *Note: The monetization of large-scale non-business real estate and other assets held since the past was completed through a series of initiatives by the fiscal year ended March 31,2026. Future classification into Category 1 and their disposal and monetization will not be conducted primarily for financial purposes, but will be continued targeting underutilized assets arising from the reorganization of our facility network in response to changes in the business environment.

4. Approach to Strategic Ownership (Views on S&LB)

The Yamato Group will not make hasty decisions to liquidate (S&LB) based solely on whether there are unrealized gains, or one-off cash generation effects.

For example, if S&LB were implemented at a core facility in a hard-to-replace location, where specialized automation equipment is integrated with the building, we could enjoy a one-off capital gain, but the facility’s operating profit could fall into the red due to the burden of substantial new rent payments, resulting in a significant deterioration of ROIC. For such facilities, we believe that maintaining strategic ownership is the rational choice, from the perspective of avoiding business continuity risks, and maximizing shareholder value (Free Cash Flow) over the medium to long term.

5. Execution Structure and Governance

To ensure transparency regarding the execution and validity of this strategy, Yamato has established the following governance framework:

- 1Integration into business plans: Formulate a roadmap for asset reorganization within future business plans, and monitor progress toward quantitative targets aimed at improving return on capital.

- 2Continuous evaluation and verification: Periodically conduct evaluation scoring for all real estate assets owned, and re-examine the rationale of holding them in light of changes in the business environment. Share and report the results at the Board of Directors meetings and other relevant bodies to ensure effective supervision.

- 3Appropriate risk management (Clean Exit): Prior to any disposal transaction, conduct thorough checks for compliance with the Fire Service Act and other relevant laws and regulations, and carry out any necessary remedial works. Ensure transactions are executed under appropriate management conditions to eliminate future legal and other associated risks.

- 4Rigorous discipline for new investments: For new capital expenditures or facility developments, set hurdle rates based on the cost of capital (WACC) from the initial planning stage and ensure a rigorous investment verification process.